The RED C Consumer Mood experiences a very slight improvement this quarter, with a reading of -31 in April 2024, a four point increase from the previous wave in January. The mood is especially low among the “squeezed middle”, particularly: women; those aged 25-54; and middle to lower socio-economic groups.

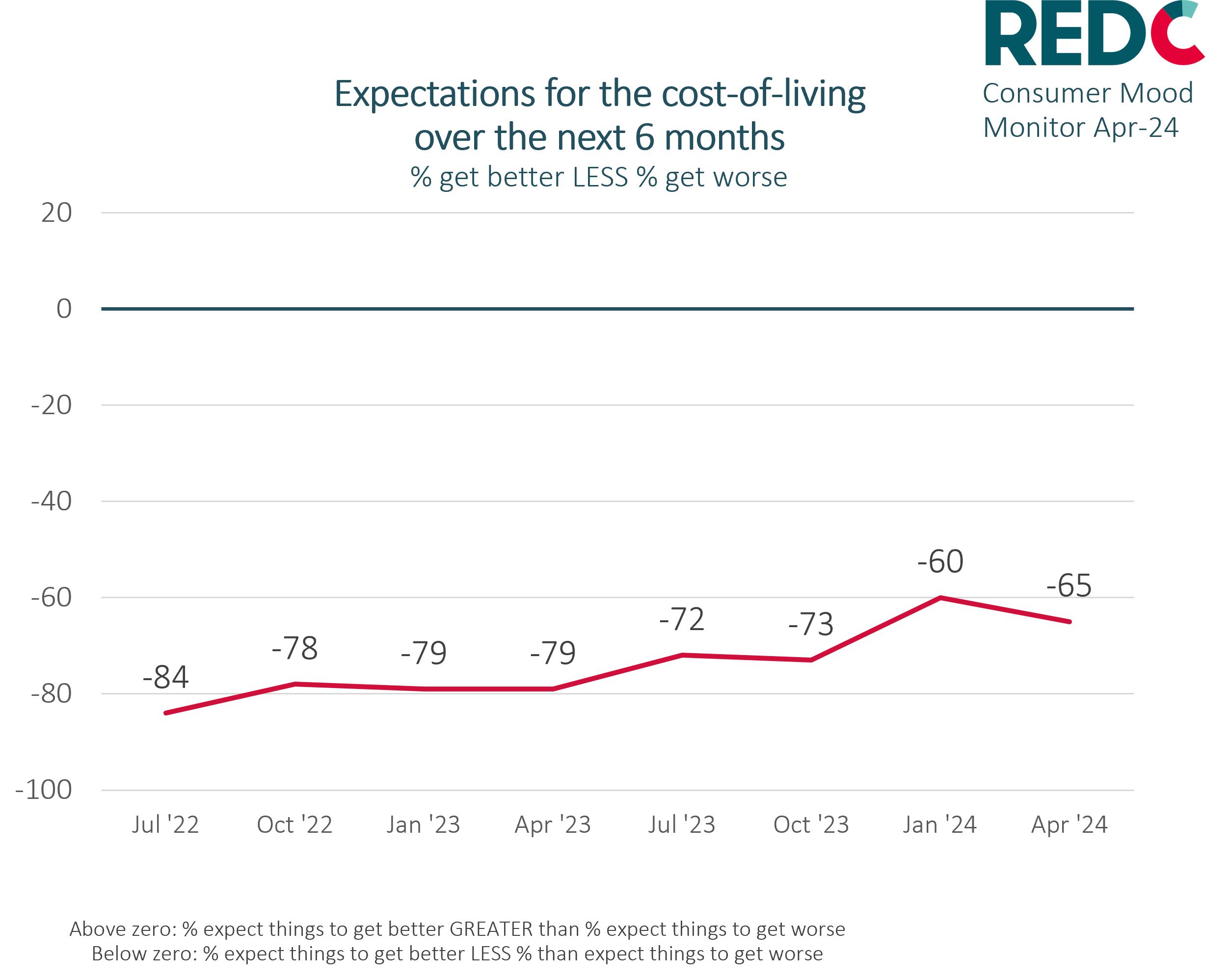

Negative consumer sentiment appears to be driven primarily by concerns around cost-of-living and the knock-on effect this has had on discretionary disposable income. While inflation appears to have slowed considerably in recent months, prices are now at higher level than before and consumers are adjusting to a new reality of living with reduced spending power.

While the cost-of-living crisis is no longer really a “crisis” per se, price increases in the areas of motor fuel, health insurance and streaming subscriptions amongst others appear to be impacting on the overall consumer mood. Geopolitical instability in the Middle East may also be having some impact (concerns over implications this may have for energy prices).

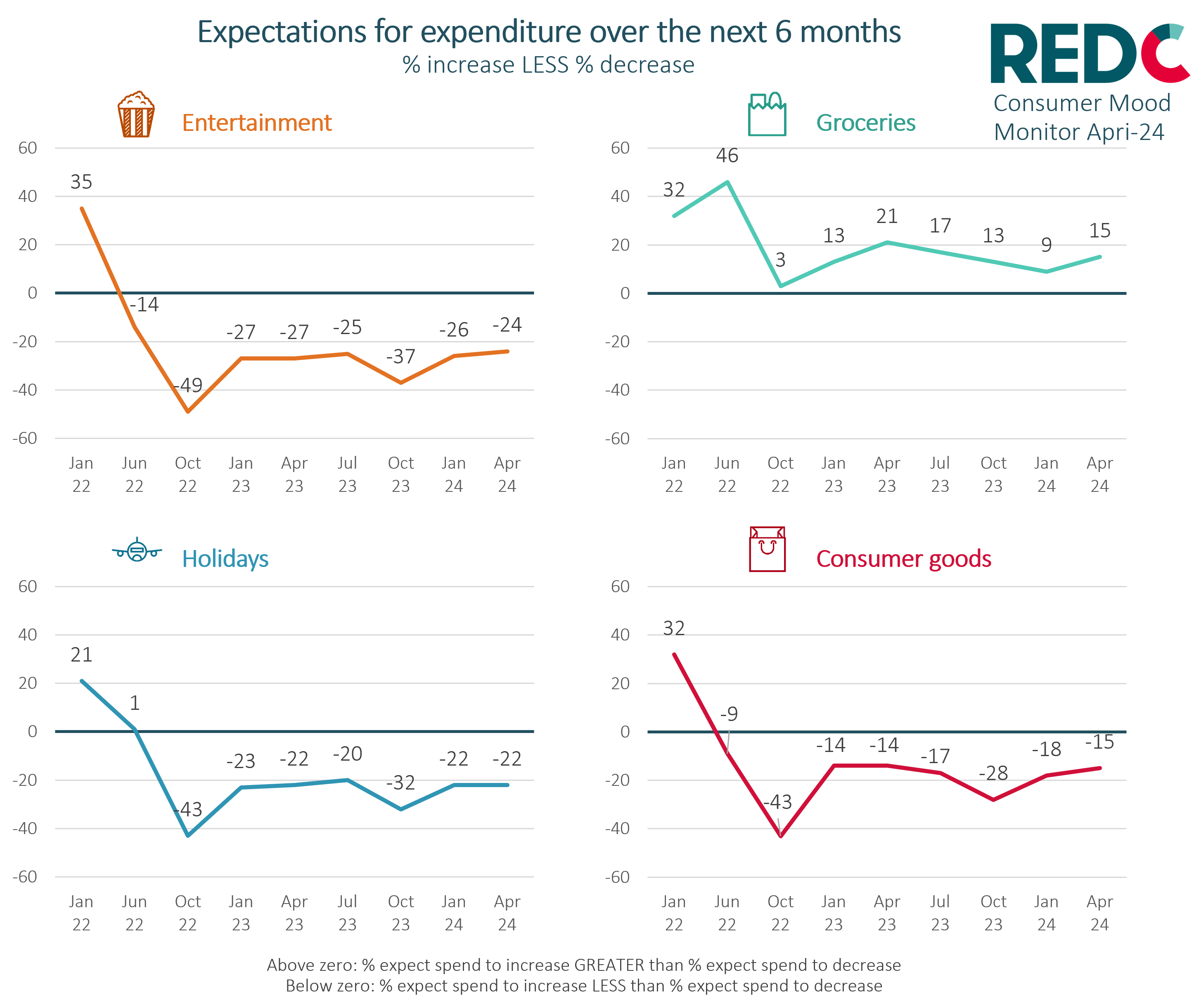

Expected spend on discretionary areas of consumer goods, entertainment and holidays looks to remain under pressure and this is already evident in CSO data showing slower growth in retail sales. This is likely to mean weaker domestic demand and overall slower economic growth.

On the whole, the “bad news” stories over the last twelve/eighteen months that have supressed consumer sentiment (mainly around the cost-of-living) appear to have declined of late, especially with inflation coming back under control. But equally, there has not been a whole lot of “good news” stories either that would give consumer confidence a sustained lift.

Not that the economy is at any great risk of being in trouble. If anything, it’s in pretty good health at the moment and the data on employment and unemployment supports this view. Also, consumers are likely to get a boost in the second half of the year with the ECB signalling that it will cut interest rates, which in turn will help reduce the cost of credit and be good news for homeowners. This, aligned with what is likely to be a generous budget heading into an election cycle, will help support incomes and potentially give a lift to consumer confidence heading into the autumn and winter months.

Building Brands

Building Brands Our Team

Our Team Our Associations

Our Associations Our Work

Our Work Where We Do It

Where We Do It Political Polls

Political Polls Latest RED C News

Latest RED C News